International payments can be a serious challenge. A small compliance error - regardless of whether or not any actual fraud or money laundering occurred - can lead to crippling penalties. So you have to invest in increased compliance, and that’s money that’s hard to recoup when you’re dealing with small volumes, often in emerging regions with incomplete or patchy regulation.

It’s hard to criticise that aim, but it’s also hard to fulfil it. You have a duty to run a commercially viable enterprise, but with downward pressure on margins and upward spiralling of risks, how do you make profit? And if it’s not economically viable to service a region, you’re criticised for derisking.

Let’s look at how this can be fixed.

All too often, cross-border payments are a to-and-fro, labour intensive and potentially risky process. It’s rare you enjoy the luxury of handling the in and out elements of a transaction; you’ll almost always be dealing with counterparties, and that’s where it all starts to get tricky. And slow. And expensive.

The problem will already be familiar. The organisation at each end onboards its client, hopefully in full compliance with regulations, but you have no control over what’s happening at the other end of the chain. The payment instruction gets passed along, usually by SWIFT, or Fedwire for American transactions. Neither has the capacity to carry much KYC information, so each stage in the payment process usually requires a request for further information. Delays build, and whole departments become absorbed in the process of requesting, providing and correlating information. Errors and omissions creep in and multiply. And everyone’s risk is increased.

You can’t rely on someone else’s compliance decisions, but making your own requires at least the information your counterparty possesses, and possibly more. But messaging systems like SWIFT and Fedwire can’t deliver everything you need. ISO20022 is a step in the right direction - if you’ve implemented it - but even that can’t show you the supporting documents.

One eKeyiD, which fits easily into a single line of the MT103 Field 70 or the Fedwire payment details gives you immediate access to the full onboarding stack. And if you still need more, the eKeyiD portal and APIs route your request directly to the person with the answers.

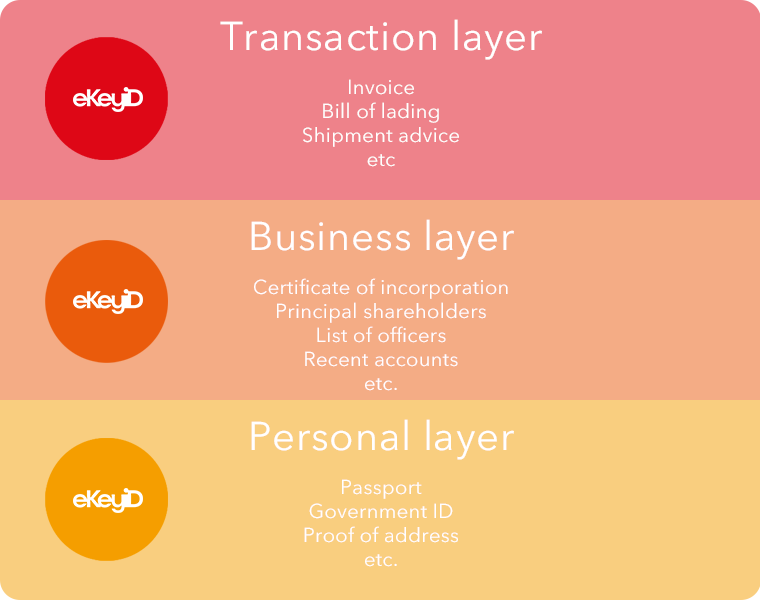

Under the eKeyiD system, payment instructions contain a transaction key. This provides access to the details of the transaction itself, such as the invoice shipping details and so on. The key gives you visibility of the purpose of funds, allowing you to assess important factors like rational market value

Most banks also have authority to access the subordinate layers of information, based on permissions granted by the subject(s) of the data. This allows you to drill down into and through the business layer, down to significant officers in the business.

If you wish, you can reduce your workload further by having the customer fuel their own onboarding process. You just set them up via your dashboard - or your own banking system if you’ve gone for API integration - and our system creates an upload request. Your customer then uses your banking app, website or our customer portal (branded to your design) to upload and maintain their documents. Either way, their entire experience matches your branding.

All data is stored by default under our patented federated ledger technology. Called DotLedger, it represents the next generation, beyond blockchain for both security, energy consumption and running costs. It can be regionalised to suit your local regulations, and your customers’ rights to privacy are baked into the architecture

CertiQi Limited

Emperor's Gate

114a Cromwell Road

London

United Kingdom

SW7 4AG

Copyright ©2026, CertiQi Limited